Limiting climate change to 2 °C will require not only a 90% reduction in global greenhouse gas emissions by 2050 but also the creation of additional C-sinks of at least 220 billion tons of carbon (800 billion tons of CO2eq) by 2100 (Hilaire et al., 2019; Rockström et al., 2017; Werner et al., 2018). Expanding biomass productivity of agricultural land through methods such as agroforestry, forest pastures, forest gardens, and algae farms could remove a total of at least 30% of the required amount of carbon from the atmosphere over the next 70-80 years. If this biomass would be converted to biochar and pyrolysis oil using pyrolysis plants (Schmidt et al., 2019), the extracted carbon could be transformed into long-term carbon sinks (centuries to millennia). However, there is still a long way to go in terms of both agricultural and industrial development to produce roughly 100 billion tons of pyrogenic carbon (biochar and pyrolysis oil) from 300 billion tons of additional biomass.

In the first decade of the biochar industry, which in Europe began in 2009 when the first pyrolysis plant dedicated to biochar production was commissioned in Switzerland, a small, dynamically evolving market has established itself. In 2012, there were only three EBC-certified plants in Germany, Austria, and Switzerland with a total production volume of just under 500 tons of biochar per year (the machines stood idle for longer than they were producing biochar). In 2021 more than 60 biochar production sites in ten European countries with an annual production of over 40,000 t of biochar are operating. The US, Canada, Australia, and China have also seen sustained growth in biochar production. The industry is professionalizing via the establishment of industry associations such as the European Biochar Industry Consortium (EBI), most producers and technology providers are active members of the International Biochar Initiative (IBI), and a growing number of countries have a national biochar association in which industry, science, government, nature conservation, and other stakeholders exchange information in order to grow national biochar industries. At the same time, the regulatory framework for using biochar in different markets is gradually becoming clearer.

C-Sink Certificates

With the introduction of the EBC C-sink certificate in 2020, the industry became a forerunner in the establishment of negative emission technologies, i.e., the creation of C-sinks. While most political and scientific decision-makers proclaimed the need for negative emissions, no other framework or certification schemes had been developed yet.

The 800 billion metric tons of CO2 (i.e., 800 Gt CO2eq) calculated according to various climate models to be permanently removed from the atmosphere by the end of the century (Hilaire et al., 2019), will almost certainly not be sufficient. On the one hand, current emissions are being reduced too slowly - despite all the noble political declarations of intent, global emissions have continued to rise. On the other hand, more and more natural carbon sinks are being destroyed or severely impaired - most notably via forest fires, thawing permafrost, and the drying out of steppes and peatlands. However, for the sake of illustrating the industrial challenge to ramp up the pyrolysis industry, we are going to use the 800 Gt CO2eq C-sink objective as a minimum target. In economic terms, this target already corresponds to a turnover of more than 500 billion euros per year assuming a price of 50 € per ton of CO2eq (= 800 billion t CO2eq / 75 years * 50 €/t). Despite this nearly unimaginable amount of both tons of CO2 and euros needed to avoid catastrophic climate change, so far there are no government initiatives to promote or mandate C-sink establishment, certification, and registry into national climate policies (apart from supporting tree plantations).

Besides the EBC-C-sink, numerous other C-sink standards are starting to emerge with more to follow in the coming years. Competition is a good driver for the further development of standards. However, in the absence of government regulation, there is a risk that the impact of certain C-sinks will be frivolously exaggerated and extrapolated to generate more supply (C-sink certificates) to meet growing demand. Currently, most large consumer product companies (e.g., cell phones, fashion, furniture, chocolate) are seeking to position themselves as carbon neutral to enhance their market image or providing their customers with the "opportunity" to offset the climate damage of their consumption for a token amount of money. To do so, these companies often look for cheap carbon credit compensation schemes that can be financed from marketing budgets. So far, these credits have mostly come from reforestation projects that have often not been subject to much scrutiny. How the land was previously used, whether and when a forest fire occurs, a pest infestation attacks the monoculture, or clear-cutting for timber use occurs after the certification period is often not factored into the carbon equation.

Considering these past experiences and the urgent need to accurately understand carbon storage, the EBC and its partners see it as their duty to set a high standard with carefully and accurately calculated and controlled carbon accounting. Future new providers of C-sink certificates will have to measure themselves using these rigorous yet transparent standards. Other carbon marketplaces that want to offer certificates based on less stringent standards will then at least have to justify the rationale for their standards, and buyers of C-sink certificates will be given comparative criteria by which they can select their C-sink providers.

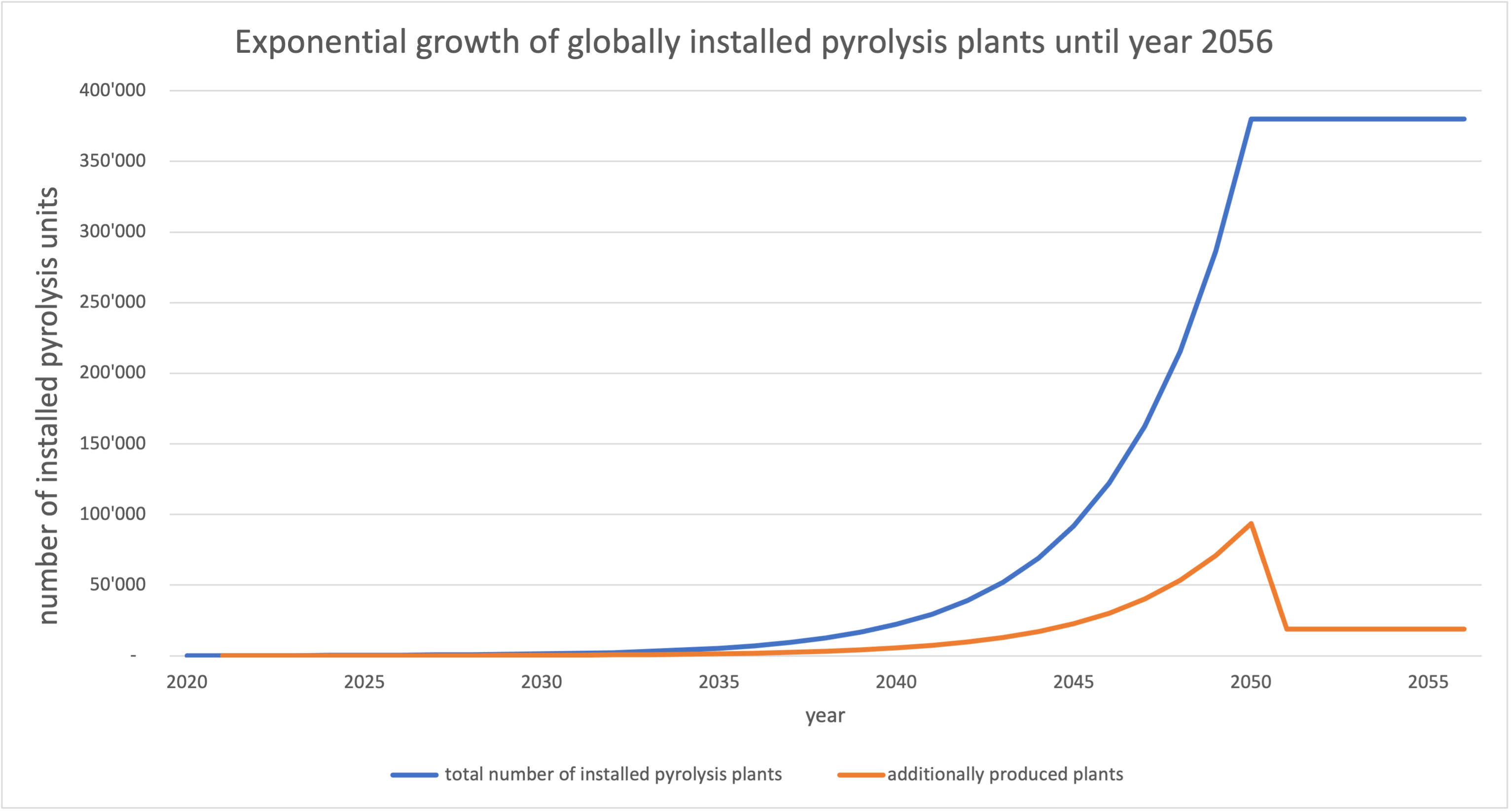

Ten years after the first EBC certification of a biochar producer, the biochar industry is about to enter a new, major, and decisive stage. Biochar pioneers, whose history will soon be written, are fast becoming industrial companies. And yet, this is admittedly a very modest and far too measured beginning. To capture at least 30 percent of the 800 billion metric tons of CO2 and store it safely and sensibly for centuries, at least 380,000 industrial pyrolysis plants will need to be built over the next 30 years.

Manufacturing of 380,000 industrial pyrolysis plants

Thirty percent of 800 billion t CO2eq corresponds to (30% * 800 billion / 44 * 12 =) 65 billion t C to be sequestered using biochar and pyrolysis oil. At a pyrolytic C efficiency of 70% (Schmidt et al., 2019), (65 * 10^9 t C / 48% C content of biomass / 70% efficiency =) 190 billion tons of biomass on a dry matter base (DM) would be required for pyrolysis. If we assume that the required technology and biomass cannot be provided at this scale before 2050, (190 billion ton / 50 years =) 3.8 billion tons of biomass (DM) will be needed per year from 2050 to 2100. A medium-sized pyrolysis plant processes an average of 10,000 tons of biomass (DM) per year to produce (10,000 t * 48% C content * 70% efficiency =) 3,400 t of sequestrable carbon. Consequently, at least (3.8 billion t biomass / 10,000 t biomass per plant =) 380,000 industrial pyrolysis plants would be needed worldwide by 2050 to fulfill the 30% goal by the end of the century.

Not only scaling up to 380,000 manufacturing plants is required, but also processes and markets must be developed to optimize and use pyrolysis oil and/or pyrolysis gas. Today, the liquid and gaseous pyrolysis products are most often simply burned to produce heat which emits CO2. If the pyrolysis oil and gas are not used for C-sequestration purposes, pyrolysis plants can only achieve 30-40% C-sink efficiencies, with a few achieving up to 50% (Schmidt et al., 2019). We have less than 30 years to achieve this scale and technology development, but given the rapid advances over the past decade, this should be achievable with the proper levels of investments.

To scale from roughly 100 industrial pyrolysis plants in 2021 to 380,000 in 2050 would require at least a 33% annual increase. Such exponential growth may not sound like much for the earlier years. It means that in the year 2030 about 320 industrial plants would have to be installed, yet by 2040 there would be a total of 22,200 installed plants, with an annual increase of 5500 plants. In 2050, if things were so mathematically exact, almost 100,000 new plants would be built annually, so that the necessary total number of 380,000 pyrolysis plants could be reached. From that moment on, however, the global biomass capacity would also be fully utilized. No new plants would be needed from this point on although older plants would have to be kept operational and replaced if necessary. This is likely to correspond to refurbishing or replacing (5% of 380,000=) 19,000 plants per year.

Fig. 1: Annual growth in installed pyrolysis plants to reach a total of 380,000 commissioned plants in 2050.

We used here a standard 10,000 tons biomass pyrolysis unit to model and illustrate the dimension of the task. We expect many different types and sizes of pyrolizers to enter the market in the next decade. It needs industrial, automatized manufacturing and serial production, but there is a need for smaller farm and village size pyrolizers (100 – 1,000 tons of biomass), mid-size pyrolizers as used in our model calculation, and big size industrial plants transforming more than 100,000 tons of biomass per year. If there will be proportionally more small-scale pyrolizers than mid- and big-scale units, the calculated 380,000 units would correspondingly be more.

Controlled shrinking

Such exponential growth followed by rapid decline is not without challenges. Starting in 2051, most of the welding robots, laser cutters, automated delivery lines, assembly halls, countless subcontractors, transport vehicles, shipping containers, company cafeterias, and, most importantly, the vast majority of the millions of workers worldwide would no longer be needed after equilibrium is reached. Of course, the workers could be retrained, and the robots reprogrammed, and the raw material flows of steel, ceramics, glass, compressed wood, and electronics redirected. But how are a company and workforce supposed to deliver plant manufacturing excellence in 2050 when the workers know they will be laid off the following year and the company knows it will have to provide warranty and service for the next 20 years on the equipment it delivers, without generating sales and profits by building new equipment?

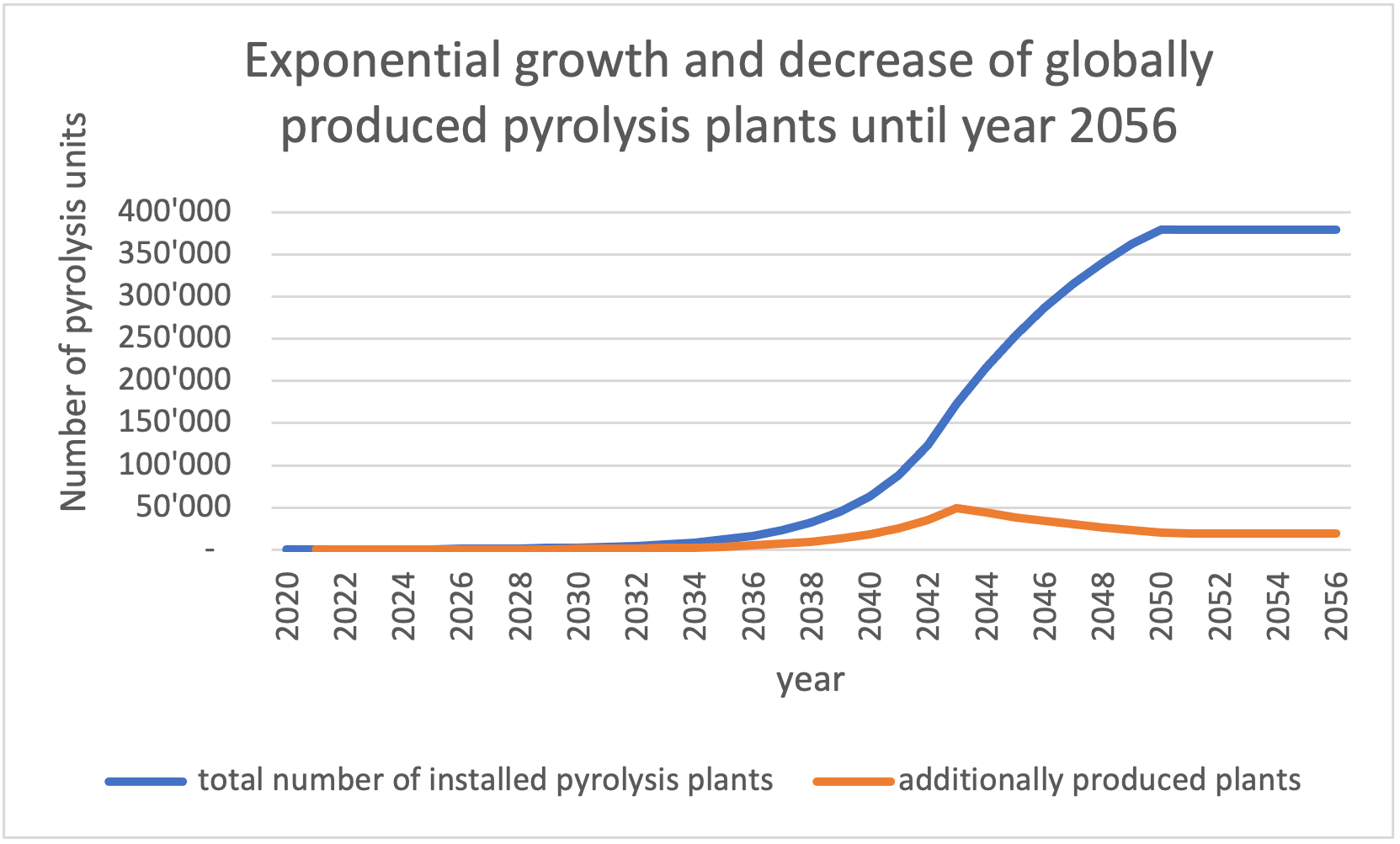

To prevent the industry, which would have been built up with high investments and commitment, from suddenly bleeding out at the moment when the target of the last 5-year plan has been reached, a slower, more orderly reduction or reallocation of production capacities should take place. However, this would also mean that the annual output of pyrolysis plants would have to proceed much faster initially so that the addition of new capacity could level off as early as 2040 and the total number of globally installed pyrolysis units would remain the same as of 2050.

As shown in Figure 2, if the annual output of pyrolysis plants from 2021 to 2043 would increase by 40% instead of 33%, the yearly output of new pyrolysis plants could decrease more slowly by 12% between 2043 and 2050. In 2050, the required 380,000 pyrolysis plants would be in operation. The continuous annual production of 19,000 pyrolysis plants would maintain the stock of installed pyrolysis capacity level until the end of the century. The manufacturing industry must be ramped up rapidly, then ramped down more slowly but still exponentially compared to current growth. Eventually, production will stabilize at a relatively low annual level. It is a fundamental economic challenge, though feasible if the appropriate policy and financial mechanisms are adopted quickly around the globe.

Fig. 2: Annual growth in installed pyrolysis capacity if there is exponential growth through 2043 and an exponential decrease in manufacturing capacity between 2043 and 2050.

This scaling challenge is not unique to pyrolysis; it is the same for all other relevant climate technologies such as direct air capture (DAC) or enhanced weathering (EW). The required industrial plants must be built quickly in large series and need exponential annual growth rates to do so, but as soon as the limits for the climate and/or the natural resources, energy, or carbon deposits are reached, the production of the climate technologies can and should be scaled down just as rapidly.

In terms of the market economy, rapid scaling followed by planned, rapid decline is a very interesting challenge: How can an exponential increase, which is necessary for climate protection, shrink again after a certain point in such a way that the planetary limits are observed, and private and national economic interests are still safeguarded. Except for a wartime economy, this type of premeditated boom and bust cycle is not something humanity has often experienced and would require nothing less than a new economic model. The purely market-based economic model, which makes the risks of a present investment appear acceptable through the expectation of future growth, would be upended. Without the planning powers of the state providing financing and social guarantees, such a massive project is very unlikely to be implemented.

Such a global targeted exponential shrinkage of a major industry had never happened before in history and was never intended. Nevertheless, there is probably no alternative when it comes to technologically countering climate change. But insofar as C-sinks can only be realized on the necessary scale within the framework of partnerships between the public sector and private industry anyway, other economic models than those valid today become conceivable.

C-sinks are based on state-regulated markets

In our view, the amount of new C-sink capacities to be created each year will have to be determined at the state or international level in accordance with the climate targets. C-sinks, like bridges, highways, railroads, wastewater pipelines, and power lines, are part of the infrastructure and should be subject to federal and international organization and management.

It should also be noted that for the following reasons, biological and pyrogenic C-sinks are not suitable for direct compensation of CO2 emissions: The residence time of organic and pyrogenic carbon in C-sinks is long but still limited (decades to millennia, depending on the type of sink), whereas historical and current CO2 emissions accumulate and exert a climate forcing for millions of years. While a carbon sink guarantees that a quantified amount of CO2 is not returned to the atmosphere for a given period of time, all CO2-emissions have a global warming effect that extends well beyond the likely survival of humankind. The climate effects of C-sinks and of CO2-emissions are not of the same temporal order. Thus, the markets, pricing, and policies for CO2 emission reductions (CO2 allowances or CO2 taxes) versus those for carbon sinks and their maintenance are fundamentally different.

Geological C sinks with residence times of many millions of years, such as the CarbFix process in Iceland or the use of rock flour for CO2 removal through geological weathering can completely compensate for emitted CO2. However, the expansion of these technologies to a climate-relevant level is expected to take several decades due to technical and physical challenges. In addition, the extraction of CO2 needed for geological storage (e.g., by DAC from Climeworks) is extremely energy-intensive, requiring further acceleration of renewable energy development. To extract one ton of CO2 from the atmosphere using DAC requires as much energy as is contained in one ton of lignite before its combustion for energy which causes one ton of CO2-emission.

In contrast, C-sinks based on organic and pyrogenic carbon can already be expanded to climate-relevant dimensions today. The fact that the carbon in such C-sinks has lower residence times than in geological C-sinks is of secondary importance over the next several decades. The decisive factor is, for now, how civilization limits climate change over the next 50 years, how the total amount of sequestered carbon increases, and how the CO2 content of the atmosphere is reduced.

The buildup of C-sinks must be an intergenerational contract. The climate problem cannot be eliminated once and for all; even centuries from now, the preservation and renewal of terrestrial C-sinks will remain an essential climate service to be carried on by future generations. While each greenhouse gas emission causes a climate effect over many hundreds of thousands of years, most C-sinks must be permanently maintained, cared for, and protected by civilization. This task can be viewed as a service contract, with duration over many generations. Following this logic, neither companies nor individuals can fully offset their past, present, and future emissions through the mere construction of a C-sink, since the services to maintain it will extend far into the future. C-sinks must be built, maintained, and their maintenance needs to be controlled and validated over generations (e.g., a biochar asphalt should not be scraped off from a road and combusted). Thus, the market and incentives for building and maintaining C-sinks should be structured differently compared to the currently existing market for emission reductions, where financial incentives to reduce emissions are created through taxes or penalties.

C-sinks require governmental and international target agreements to achieve the global amounts of necessary C-sinks identified by climate science. For example, the EU could specify a C-sink capacity target of 30 billion tons CO2eq by 2050 and a total of 230 billion tons CO2eq by 2100. Since the EU is responsible for about 29% of global climate change, it would have to pay for 29% of the necessary negative emissions of 800 Gt CO2eq, which is just under 230 billion tons CO2eq (Hickel, 2020).

If countries set binding targets for the creation of C-sinks every five years and put their request for carbon removal proposals out to tender in the same way as other public contracts, e.g., the construction of a bridge or the operation of local public transport, they could create a strong, long-term market for C-sinks while also setting up regulations to minimize double counting and promote maximum carbon efficiency. Dynamic pricing for C-sink services would emerge when the creation and assessment of C-sinks follow internationally binding agreements. Public tender creates competition to develop C-sinks as large as possible, as long-term as possible, and as cost-effectively as possible. Direct or indirect taxes should be leveraged to finance the creation and maintenance of C-sinks. C-sinks are not ordinary products from which a consumer or a company has a direct physical benefit like when a van is purchased that can transport goods or a computer the allows internet surfing. The real benefit of setting up C-sinks is reversing climate change, but that will only occur if the entire global community participates. The private benefit only occurs

Without the participation of all, individual actions will only have a minimal effect, barely measurable in the grand scheme of planetary emissions. C-sinks are part of civilization's responsibility and must therefore be organized and financed by the peoples' representatives, i.e., countries. Thus, nation-states would be both the end customer buying the climate service of a C-sink and the initiator supporting the establishment of the industry through co-financing new production capacity. Much of this investment money could and should come from CO2 taxes. It is evident that carbon taxes must be generated mainly in wealthy industrialized countries and must include their respective historical responsibility for climate change (Hickel, 2020). Due to the long residence time of CO2 in the atmosphere, historical emissions (since the beginning of industrialization) are as relevant as current emissions.

CO2 credits and taxes work like a tipping or disposal fee. The objective is to make the emission of greenhouse gases gradually more expensive than the cost to avoid emissions. In order to maximize the impact of carbon taxes, the revenues generated from CO2 taxes must be invested in climate technologies. Using the CO2 taxes, the government could issue price guarantees for C-sinks and provide the necessary subsidies for constructing production lines for climate technologies. Such government involvement could also ease the impact of the anticipated exponential decrease of production capacities around mid-century. Aligning the scaling of climate removal technologies with CO2 tax rates and revenues could correspond well with the anticipated scaling timelines. The revenues from CO2 taxes will increase until about 2040 (on the one hand, by increasing the CO2 price, but mainly by gradually including all GHG emissions instead of only those of selected industries). From 2040 onwards, CO2-tax income will likely begin to decrease because, according to the Paris Climate Agreement, emissions will have to be reduced by 90% by 2050 and, thus, there would be fewer CO2-emissions to be taxed. This timeline would correspond to a decreasing growth of, and subsidies needed for pyrolysis plants production from 2043 onward.

Our civilization's capacity to compel exponential growth and targeted exponential shrinking is very likely to be a determining factor as to whether humanity will preserve our habitat in the coming decades. The climate targets adopted by almost all countries will only be achievable if the extraction of fossil carbons is exponentially reduced to a minimum. In parallel, the production of renewable energy and renewable plastics (10% of the fossil carbon extracted annually is used in plastics and chemical industries and must be replaced when fossil carbon extraction ends) must be ramped up dramatically. Economic integration of industrial shrinkage and linking it to the rapid growth of new technologies requires innovative business models, as well as social and economic reform.

Manufacturing service provider

The ramp-up and ramp-down of entire industries would have been an almost unsolvable problem in the old economy. But the more intelligently the automation of production processes is organized, the easier it will be to switch from one production line to another with the same robots, each with only short changeover phases. For example, a large factory (Gigafactory) that produces pyrolysis plants in series could build plants for direct air capture or seawater desalination or tidal power plants after a changeover phase of just three to four months. In the electronics industry, valuable experience is already being gained with flexible production lines.

Machine manufacturing is becoming increasingly modular and, at the same time, more flexible. There will be a whole new type of factory that sees itself primarily as a manufacturing service provider. Car companies, pyrolysis developers, battery manufacturers, or hydrogen producers will be able to order their equipment from manufacturing service providers in any quantity. Once the order is processed, the manufacturing service provider will switch over and fabricate different equipment for another company. This works not entirely different than it does today, where international technology companies have their products manufactured in South East Asia and sign unit contracts with the outsourced manufacturing company. The main difference could be that in the future, there will probably be less outsourcing to distant foreign countries to improve local and regional resiliency against supply chain interruptions due to climate-induced disruptions. Instead, industries are more likely to engage nearby manufacturing service providers who, with robotics, 3D printing, innovative flexibility, and precision planning, will be able to handle large orders with exponential growth rates. The flexibility of various production lines means that exponential ramp-ups and ramp-downs will be part of their daily business.

Outlook

As complex and contrary to our economic-political experiences the necessary ramp-up and orderly ramp-down of global environmental technologies may seem, there can be no doubt that the fabrication and commissioning of nearly 400,000 pyrolysis plants should be technologically and politically manageable. More problematic is the doubling of the net biomass productivity in terrestrial and marine ecosystems to facilitate increased carbon removal from the atmosphere, eventually converted to solid and liquid pyrogenic carbon products suitable for long-term carbon sequestration. If large-scale industrial methods were used to doubled biomass production, ecosystems, groundwater, and biodiversity would very likely be endangered or destroyed to an unprecedented extent (due to monoculture cropping, excessive use of fertilizers, irrigation, and massive use of pesticides).

Given the much greater potential for biomass production in the tropics, a large part of the additional biomass will have to be grown in tropical countries. Done poorly this could lead to a potentially fatal competition between food and biomass production similar to what has previously happened with the production of biofuel feedstock. It could shatter the social cohesion in regions that are already noticeably affected by climate change. We will address this potentially even greater challenge than industrial scaling in the second part of this article.

Literature

Hickel, J., 2020. Quantifying national responsibility for climate breakdown: an equality-based attribution approach for carbon dioxide emissions in excess of the planetary boundary. Lancet. Planet. Heal. 4, e399–e404. https://doi.org/10.1016/S2542-5196(20)30196-0Hilaire, J., Minx, J.C., Callaghan, M.W., Edmonds, J., Luderer, G., Nemet, G.F., Rogelj, J., del Mar Zamora, M., 2019. Negative emissions and international climate goals—learning from and about mitigation scenarios. Clim. Change 157, 189–219. https://doi.org/10.1007/s10584-019-02516-4

Rockström, J., Gaffney, O., Rogelj, J., Meinshausen, M., Nakicenovic, N., Schellnhuber, H.J., 2017. A roadmap for rapid decarbonization. Science (80-. ). 355.

Schmidt, H.-P., Anca-Couce, A., Hagemann, N., Werner, C., Gerten, D., Lucht, W., Kammann, C., 2019. Pyrogenic carbon capture and storage. GCB Bioenergy 11. https://doi.org/10.1111/gcbb.12553

Werner, C., Schmidt, H.-P., Gerten, D., Lucht, W., Kammann, C., 2018. Biogeochemical potential of biomass pyrolysis systems for limiting global warming to 1.5 °c. Environ. Res. Lett. 13. https://doi.org/10.1088/1748-9326/aabb0e

No analysis of inputs, fossil fuel subsidy to pyrolysis industry ramp up

As we close in on the reality of runaway climate change and COP 26 we will be doing more and more rear view analysis of what could have been done. Thank you HPS for your work all these years to bringing biochar to a commercially and scientifically respectable status. I read this paper through, am pretty aware of biochar claims and benefits, and am always looking for the ways through the bottleneck created by industrial civilization (Bottleneck, William Catton, 2009) So what's not to like about Hans-Peter's paper? Surely we need carbon drawdown and sequestration. Surely there are millions of hectares of dead and dying forests (due to bark beetle infestations due to climate change), surely soil remediation, water table restoration, afforestation, stabilized hydrology, (soil carbon sponge) are critical worldwide. I would have liked to see the energy input/output balance for manufacturing 400K pyro plants, the process energy costs including transport of raw biomass and distribution of end products, and a recognition of the fossil fuel dependence of this solution element to carbon pollution. Isn't the ultimate problem population overshoot and habitat destruction, of which climate change is but one symptom? As Rees and Seibert write: (https://www.mdpi.com/1996-1073/14/15/4508) Through the Eye of a Needle: An Eco-Heterodox Perspective on the Renewable Energy Transition.Energies 2021, "Humanity must embark on a planned, voluntary descent from a state of overshoot to a steady-state harmonic relationship with the ecosphere—in just a decade or two." Every solution proposed must be looked at through this lens. not only would there be a logistical discontinuity in decommissioning plants in 2050, there would be a massive carbon emissions debt accumulated through the supply and infrastructure chain, and competition for scarce mineral inputs, think steel, that should be accounted for. Indeed an intractable problem.